Investing in bonds can be a smart way to diversify your portfolio and secure a steady income stream. However, not all bonds are created equal. The safety and profitability of a bond largely depend on its bond rating. Understanding bond ratings can help you make informed decisions and choose bonds that align with your risk tolerance and financial goals.

In this detailed guide, we will explain what bond ratings are, how they work, and how to use them to select safe and profitable bonds in 2024.

What Are Bond Ratings?

Bond ratings are evaluations of a bond issuer’s creditworthiness. These ratings reflect the issuer’s ability to meet debt obligations, including paying interest and repaying the principal amount at maturity. Higher-rated bonds are considered safer, while lower-rated bonds carry a higher risk of default.

Bond rating agencies—such as Moody’s, Standard & Poor’s (S&P), and Fitch Ratings—assign these ratings based on a thorough analysis of the issuer’s financial health, market conditions, and other factors.

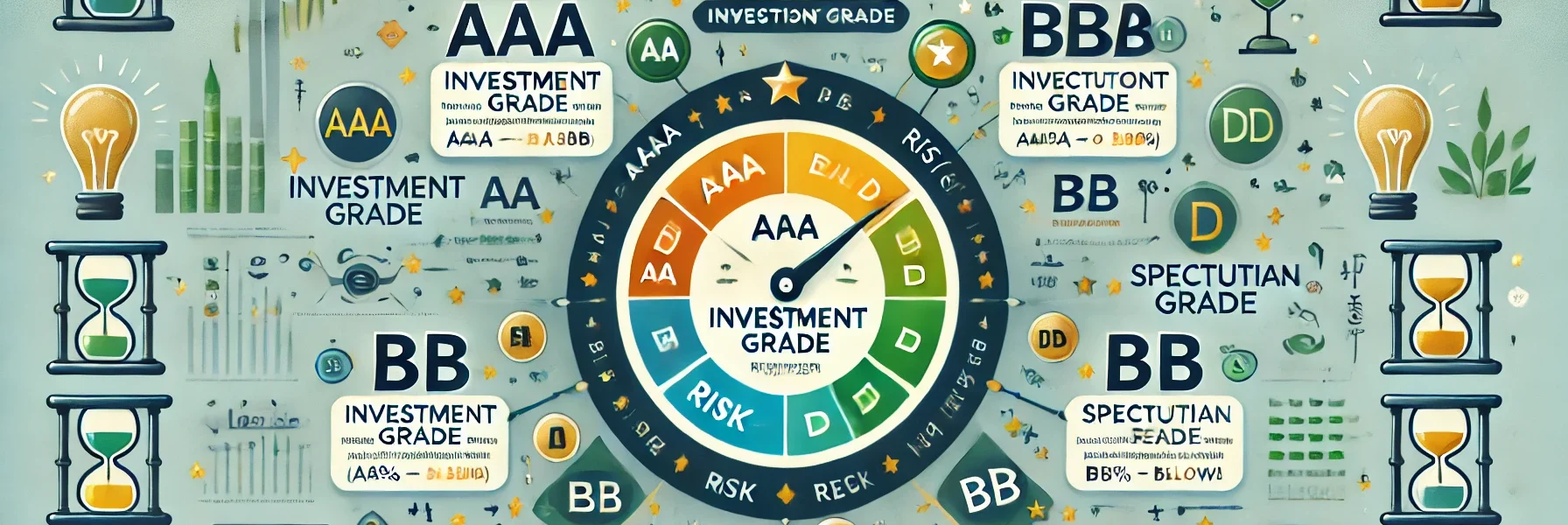

Common Bond Rating Scales:

| Rating Agency | Investment Grade (Safer) | Speculative Grade (Riskier) |

|---|---|---|

| Moody’s | Aaa, Aa, A, Baa | Ba, B, Caa, Ca, C |

| S&P | AAA, AA, A, BBB | BB, B, CCC, CC, C, D |

| Fitch | AAA, AA, A, BBB | BB, B, CCC, CC, C, D |

Investment-grade bonds (AAA to BBB) are lower risk and suitable for conservative investors, while speculative-grade bonds (BB and below), also known as junk bonds, offer higher returns but come with greater risk.

Why Are Bond Ratings Important?

- Assessing Risk: Bond ratings help investors understand the likelihood of receiving regular interest payments and getting their principal amount back.

- Comparing Bonds: Ratings provide a standardized way to compare bonds from different issuers.

- Portfolio Diversification: Understanding ratings enables investors to balance high-risk and low-risk investments.

- Interest Rate Prediction: Lower-rated bonds typically offer higher interest rates to compensate for increased risk.

How Are Bond Ratings Determined?

Rating agencies evaluate several factors to assign bond ratings, including:

- Financial Health of the Issuer: Revenue, profit margins, cash flow, and debt levels.

- Economic Conditions: The broader economic environment and its impact on the issuer.

- Industry Outlook: The sector’s stability and future growth potential.

- Management Quality: The issuer’s leadership and decision-making capabilities.

- Default History: Past record of meeting debt obligations.

Understanding the Risks Associated with Different Bond Ratings

- AAA and AA Bonds (Highest Quality): Extremely safe investments with low risk of default. Ideal for conservative investors.

- A and BBB Bonds (Investment Grade): Moderate risk with slightly higher yields. Suitable for balanced portfolios.

- BB and B Bonds (Non-Investment Grade): Higher risk, but offer better returns. Best for aggressive investors willing to accept volatility.

- CCC and Below (Highly Speculative): Significant default risk. Suitable for experienced investors looking for high-yield opportunities.

How to Choose Safe and Profitable Bonds

1. Evaluate Your Risk Tolerance

- Low-Risk Investors: Stick to AAA, AA, or A-rated bonds.

- Moderate-Risk Investors: Consider BBB bonds for a balance between safety and returns.

- High-Risk Investors: Explore BB and B-rated bonds for higher returns but be aware of potential losses.

2. Analyze Bond Duration and Maturity

- Short-Term Bonds (1-3 years): Lower risk and less affected by interest rate changes.

- Medium-Term Bonds (3-10 years): Moderate risk and yield.

- Long-Term Bonds (10+ years): Higher returns but vulnerable to interest rate fluctuations.

3. Consider Bond Types

- Government Bonds: Backed by the government, offering maximum security.

- Corporate Bonds: Higher returns but carry credit risk.

- Municipal Bonds: Tax-free and suitable for long-term savings.

- High-Yield Bonds: Offer higher interest but come with substantial risk.

4. Research Bond Issuers

Examine the issuer’s financial statements, past performance, and market position. Strong issuers are less likely to default.

5. Understand Yield vs. Risk Trade-Off

- Higher-rated bonds = Lower yields, more safety

- Lower-rated bonds = Higher yields, greater risk

How to Interpret Rating Changes

Bond ratings are not static and can change based on the issuer’s performance and market conditions. Be mindful of:

- Upgrades: Indicate improving creditworthiness and reduced risk.

- Downgrades: Signal increased risk and potential default.

Monitoring rating changes helps you make timely decisions about holding or selling bonds.

Tools and Resources for Evaluating Bond Ratings

- Official Rating Agency Websites: Moody’s, S&P, and Fitch provide real-time rating data.

- Financial News Platforms: Stay updated on rating changes and market conditions.

- Bond Screeners: Use online tools to filter bonds by rating, yield, and maturity.

Common Mistakes to Avoid When Choosing Bonds

- Chasing High Yields: Avoid focusing solely on returns without considering credit risk.

- Ignoring Rating Changes: Pay attention to bond upgrades or downgrades.

- Overconcentration: Diversify across different ratings, sectors, and maturities.

- Neglecting Liquidity Needs: Ensure the bond’s maturity aligns with your financial goals.

Conclusion: Making Informed Bond Investments

Understanding bond ratings is crucial for making informed investment decisions. By assessing bond ratings, evaluating your risk tolerance, and staying informed about rating changes, you can build a safe and profitable bond portfolio.

In 2024, as market conditions evolve, being proactive and thorough in your research will ensure that you choose bonds that offer both security and attractive returns.

Always consult a financial advisor before making any investment decisions to ensure your choices align with your financial goals and risk appetite.