In recent years, cryptocurrencies have emerged as a revolutionary force in the financial world, offering new opportunities for individuals and businesses alike. But beyond the hype and speculation surrounding digital currencies like Bitcoin and Ethereum, one of the most exciting and impactful aspects of cryptocurrency is its potential to promote financial inclusion. In this blog, we will explore how cryptocurrencies are playing a critical role in bringing financial services to underserved populations and contributing to global economic equality.

1. What Is Financial Inclusion?

Financial inclusion refers to the access and availability of basic financial services, such as savings accounts, credit, insurance, and payments, for all individuals and businesses, particularly those in underbanked or underserved communities. Despite advancements in global financial systems, billions of people around the world still lack access to these essential services. The reasons for this lack of access are diverse, ranging from geographical isolation and poverty to the exclusion of certain groups based on gender, race, or economic status.

Inclusion is a key driver of economic development. When people have access to financial services, they can save money, invest in businesses, manage risk, and improve their overall quality of life. Cryptocurrencies, with their decentralized nature and borderless access, have emerged as a potential solution to this longstanding problem.

2. How Cryptocurrency Promotes Financial Inclusion

Cryptocurrency offers a host of advantages that can support financial inclusion, especially in regions where traditional banking infrastructure is limited or unavailable. Let’s dive into the specific ways in which cryptocurrency can bridge the gap and provide access to financial services:

a) Decentralized Access to Financial Services

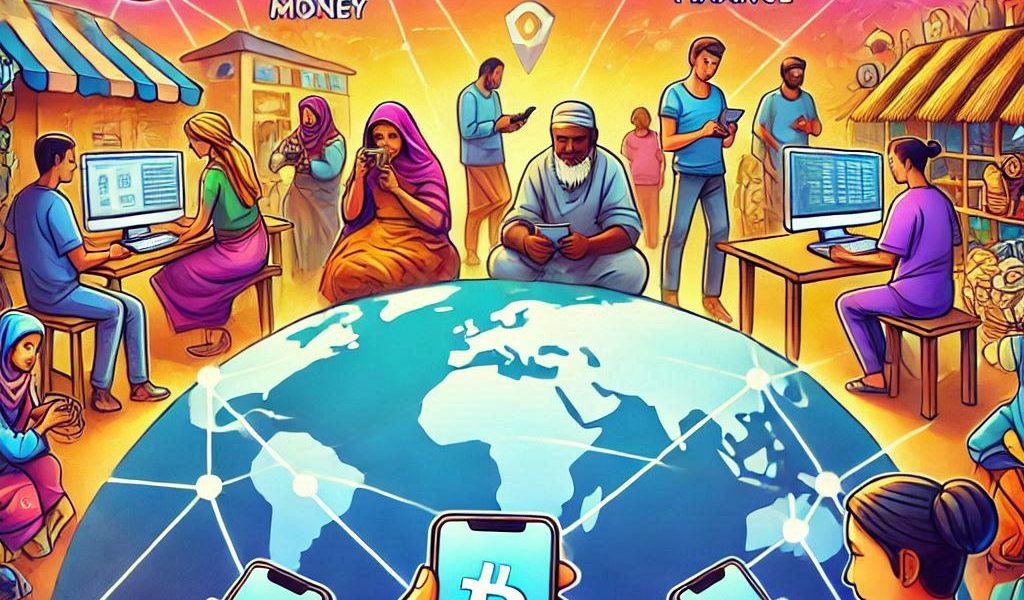

One of the primary features of cryptocurrencies is decentralization, meaning they are not controlled by any government or financial institution. This allows individuals in regions with limited access to traditional banking systems to directly participate in the global economy. All that is needed is an internet connection and a smartphone.

For example, people in developing countries can use cryptocurrencies to send and receive money, buy goods and services, and invest—without the need for a bank account or a credit history. This eliminates the barriers imposed by centralized banks, such as high fees, long wait times, and geographical limitations.

b) Affordable Cross-Border Transactions

International money transfers can be costly, especially for people in developing nations. Traditional remittance services, like Western Union or MoneyGram, often charge high fees for sending money across borders, with a significant portion of the transaction going to intermediaries.

Cryptocurrencies offer a solution by enabling peer-to-peer transactions that bypass intermediaries. This makes sending money across borders much more affordable and accessible. For example, using Bitcoin or stablecoins like USDC, individuals can transfer funds at a fraction of the cost compared to traditional remittance services, helping to facilitate global financial inclusion.

Additionally, cryptocurrencies enable near-instantaneous transactions, reducing the time delays that often occur with traditional banking systems. This can be particularly beneficial for people who need quick access to their funds in emergencies.

c) Banking the Unbanked

Around 1.7 billion people worldwide remain unbanked, meaning they do not have access to any form of formal financial services. This can be due to a lack of banking infrastructure, insufficient funds to open accounts, or other social and economic barriers. Cryptocurrencies can help bank the unbanked by offering them an easy entry point into the financial system.

By using a mobile wallet or cryptocurrency exchange, individuals can hold, send, and receive cryptocurrencies without needing a physical bank account. This provides financial services to people who may have otherwise been excluded from the traditional banking system, especially in remote or rural areas where brick-and-mortar banks are not present.

d) Access to Microloans and Peer-to-Peer Lending

Cryptocurrency platforms are also playing a role in financial inclusion by offering access to microloans and peer-to-peer lending services. In many parts of the world, individuals in need of small loans often struggle to access credit from traditional banks due to lack of collateral or a formal credit history.

Crypto-based lending platforms allow people to lend and borrow money directly from others, often without the need for intermediaries. Additionally, DeFi (Decentralized Finance) protocols offer decentralized lending and borrowing, providing individuals with the ability to take out loans using cryptocurrency as collateral.

These platforms enable greater financial empowerment for those in underserved communities, helping individuals access capital to start businesses, pay for education, or invest in their future.

3. Stablecoins: The Key to Financial Stability

One of the key challenges that many cryptocurrencies face, particularly in regions with high inflation or economic instability, is price volatility. Cryptocurrencies like Bitcoin can fluctuate wildly in value, making them impractical for everyday use in some situations.

However, stablecoins—cryptocurrencies that are pegged to the value of a stable asset like the US dollar—provide a more stable alternative. Stablecoins like Tether (USDT) and USD Coin (USDC) can be used to store value and conduct transactions without the fear of sudden value swings.

For individuals in countries experiencing hyperinflation or unstable currencies, stablecoins provide a secure means of saving and transferring money. This can reduce the reliance on traditional fiat currencies, which may be subject to rapid devaluation.

4. Cryptocurrency as an Enabler of Economic Empowerment

Cryptocurrency isn’t just about sending and receiving money—it’s also about empowering individuals to take control of their financial futures. For those living in areas with limited economic opportunities, cryptocurrency can provide an alternative means of generating income through staking, mining, and investing.

For instance, people in economically disadvantaged regions can use cryptocurrency to earn passive income by participating in staking or yield farming. These activities can offer returns without requiring large initial investments, helping people build wealth over time.

Additionally, blockchain-based platforms allow individuals to create and manage smart contracts, run decentralized applications (dApps), and access various financial services without relying on banks. These tools foster entrepreneurship and innovation, giving people new avenues to generate income and improve their financial standing.

5. Challenges to Widespread Financial Inclusion

While cryptocurrencies hold tremendous promise in driving financial inclusion, there are still challenges that need to be addressed:

- Internet access: To use cryptocurrencies, individuals need reliable internet access and smartphones, which are not available to everyone, especially in rural areas.

- Education and awareness: Many people are still unaware of how cryptocurrencies work and how they can use them. Education and outreach efforts are crucial to ensuring that cryptocurrencies fulfill their potential in promoting financial inclusion.

- Regulation: The lack of clear regulatory frameworks in many countries can deter people from adopting cryptocurrencies, as they may fear fraud, scams, or legal complications.

- Volatility: As mentioned earlier, the volatility of cryptocurrencies can undermine their effectiveness in providing stable financial solutions for those in vulnerable economic situations.

6. Conclusion: The Future of Cryptocurrency and Financial Inclusion

Cryptocurrencies have the potential to transform the financial landscape by providing greater access to financial services for underserved populations worldwide. With their decentralized nature, affordable cross-border transactions, and ability to facilitate microloans and peer-to-peer lending, cryptocurrencies offer a powerful tool for promoting financial inclusion.