Investing in bonds is a popular way to generate fixed income while preserving capital. However, to make informed decisions, investors must carefully analyze the bond prospectus—a legal document that outlines key details about the bond offering. Understanding the prospectus helps investors assess the risk, return, and suitability of the bond in their investment portfolio.

In this comprehensive guide, we will break down how to analyze a bond prospectus step-by-step to ensure you make educated investment decisions.

What is a Bond Prospectus?

A bond prospectus is a formal legal document issued by the bond’s issuer, providing essential information to potential investors. It is required by regulatory authorities (e.g., the Securities and Exchange Commission in the U.S.) to ensure transparency and protect investors.

The bond prospectus typically includes:

- Details of the bond offering

- Financial health of the issuer

- Terms and conditions

- Risk factors

- Legal obligations

Why is Analyzing a Bond Prospectus Important?

Understanding a bond prospectus allows investors to:

- Evaluate the creditworthiness of the issuer

- Assess the potential risks and rewards

- Understand payment terms and conditions

- Avoid misleading investments

Step-by-Step Process to Analyze a Bond Prospectus

1. Identify Key Bond Features

Start by reviewing the bond’s fundamental characteristics, which are usually listed in the opening section.

- Issuer: Identify the company, government, or organization issuing the bond.

- Bond Type: Determine whether it is a government, corporate, municipal, or international bond.

- Coupon Rate: Understand the fixed or floating interest rate paid to investors.

- Maturity Date: Note when the bond will mature, and the principal will be repaid.

- Face Value (Par Value): Identify the amount the bondholder will receive upon maturity.

Example: A corporate bond with a 5% annual coupon rate, maturing in 10 years, and a face value of $1,000.

2. Examine Interest Payment Structure

Bonds can have different payment schedules and structures.

- Fixed-Rate Bonds: Pay a consistent interest rate throughout the bond’s life.

- Floating-Rate Bonds: Interest rates vary based on benchmark rates (e.g., LIBOR).

- Zero-Coupon Bonds: No periodic interest; issued at a discount and paid in full at maturity.

Understand how frequently payments are made (monthly, quarterly, semi-annually, or annually).

3. Analyze Credit Ratings and Risk Assessment

Credit ratings indicate the issuer’s ability to meet financial obligations. These ratings are provided by agencies like Moody’s, S&P Global, and Fitch.

- Investment-Grade Bonds: Rated BBB- or higher, indicating lower risk.

- High-Yield (Junk) Bonds: Rated below BBB-, indicating higher risk and potential returns.

Tip: Always cross-check ratings from multiple agencies for a comprehensive view.

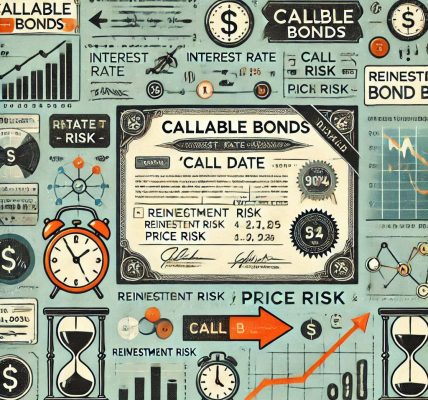

4. Understand Call and Put Provisions

- Callable Bonds: The issuer can redeem the bond before maturity, which can affect long-term returns.

- Puttable Bonds: Investors can sell the bond back to the issuer before maturity.

Example: A bond callable after five years may be redeemed if interest rates drop, reducing future interest payments to investors.

5. Review Financial Information and Covenants

The prospectus includes financial statements and legal covenants that outline the issuer’s obligations.

- Debt-to-Equity Ratio: Measures the issuer’s leverage and ability to repay debt.

- Interest Coverage Ratio: Indicates the issuer’s capacity to pay interest.

- Restrictive Covenants: Conditions imposed on the issuer to protect bondholders (e.g., limits on issuing more debt).

6. Evaluate Risk Factors

The risk section details potential threats to the bond’s value or payment structure.

Common risks include:

- Credit Risk: The possibility of issuer default.

- Interest Rate Risk: Bond prices fall when interest rates rise.

- Inflation Risk: Reduced purchasing power due to inflation.

- Liquidity Risk: Difficulty in selling the bond in the secondary market.

Tip: Pay close attention to industry-specific risks and economic conditions.

7. Legal and Tax Considerations

Understand the legal framework and tax implications of the bond investment.

- Jurisdiction: The legal environment governing the bond.

- Tax Status: Municipal bonds may offer tax-free interest income, while corporate bonds are usually taxable.

Example: A U.S. Treasury bond is exempt from state and local taxes but subject to federal taxation.

8. Compare Yields and Market Conditions

Yields determine the bond’s profitability. Evaluate the following metrics:

- Nominal Yield: Annual coupon payment divided by face value.

- Current Yield: Annual coupon payment divided by current market price.

- Yield to Maturity (YTM): Total return if the bond is held until maturity, including interest payments and capital gains/losses.

Compare these yields with similar bonds and broader market conditions to assess competitiveness.

9. Investigate Redemption and Default History

Check the issuer’s track record for timely payments and adherence to legal obligations.

- Default History: Frequent defaults indicate higher risk.

- Redemption Patterns: Frequent early redemptions may indicate potential interest rate changes.

10. Make an Informed Decision

After analyzing all aspects of the bond prospectus:

- Weigh the risks against potential returns.

- Ensure alignment with your investment objectives.

- Diversify across bond types to mitigate individual bond risks.

Final Thoughts

A thorough review of the bond prospectus is essential for informed investment decisions. By understanding the issuer’s financial health, legal obligations, and market conditions, investors can mitigate risks and optimize their returns.

Whether you’re a novice or an experienced investor, following this step-by-step guide ensures a comprehensive evaluation of bond offerings, allowing you to make decisions confidently and safely.